With tuition, textbooks, rent, and daily expenses piling up, the constant need for money can push you toward quick financial fixes.

But behind those easy approvals and flashy promises are subprime financial products designed to hook you and drain your wallet. These products aren’t just bad deals—they’re traps posing as lifelines. Recognizing them is the first step to avoiding a debt spiral that’s hard to escape.

Buy Now Pay Later

Buy Now Pay Later (BNPL) programs let you split purchases into interest-free payments, which seems ideal when you’re living paycheck to paycheck. Companies like Afterpay, Klarna, Affirm, and Sezzle dominate this space, offering easy approvals and quick checkout options at popular retailers. Miss a payment, and late fees add up quickly. Some BNPL providers even report it to credit bureaus, damaging your credit score. Additionally, confusing terms and hidden processing fees make it easy to overspend without realizing the true cost.

Let’s break it down.

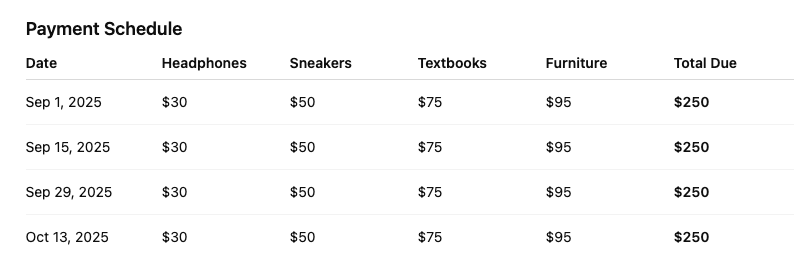

You might use BNPL services like Afterpay, Klarna, or Affirm for headphones ($120), sneakers ($200), textbooks ($300), and dorm furniture ($380). That’s $1,000 in spending, split into four payments over six weeks instead of paying upfront. Let’s break it down and assume there’s no interest due.

That’s $500 a month for the next 2 months. While BNPL feels cheap (just $30 today!), the cost overlapping purchases piles up. Fees for missed payments can run up to $35 per item.

Credit Builder Loans

Credit builder loans aren’t inherently bad, but many come with high fees or require locking up your own money. Companies like Self Financial and Credit Strong target people with little or poor credit, yet some charge for services like credit reporting—something you can often do for free. Choosing reputable lenders with clear, transparent terms is crucial to avoid paying extra for a simple way to build credit.

Payday Loans

Traditional payday lenders like CashNetUSA, ACE Cash Express, and Speedy Cash offer short-term, high-cost loans designed to be repaid on your next payday. They often market “no credit check” and fast approval, but the fees are astronomical—APRs frequently exceed 300%. A $500 loan can cost $75 or more in fees for just two weeks. If you can’t repay quickly, you may roll the loan into a new one with more fees, trapping you in a cycle of debt that’s nearly impossible to escape without paying far more than you borrowed.

When you take the loan, you either write a post-dated check or authorize an electronic debit for the amount due plus fees. On your due date, they withdraw the money directly. If there aren’t enough funds, they still try to collect, which can trigger overdraft fees and add to the borrower’s costs.

Rent-to-Own Plans

Companies like Rent-A-Center, Aaron’s, and Buddy’s Rental offer rent-to-own agreements where you can take home electronics, furniture, or appliances with low weekly or monthly payments. The catch is that the total cost often ends up two to three times the retail price, and missing a payment means you can lose the item with no equity built. You’re effectively renting the product, but “owning” it is usually only realistic if you commit long term.

For example, the latest laptop model is $900 to buy outright. Instead, a rent-to-own plan feels affordable at $35 a week. At first, it seems like a win because you walk out with the laptop the same day. But after six months of weekly payments, you’ve already paid over $900—and still doesn’t own it. By the time the contract ends, you may have shelled out nearly $1,800 for a $900 laptop. If you misses a payment, the store can repossess the laptop, leaving you with no computer and no refund for what already paid.

Title Pawning: Gambling Your Ride for Cash

Title pawning companies such as TitleMax, LoanMax, and Auto Credit Express offer loans using your vehicle title as collateral, often charging interest rates exceeding 200% APR. While it seems like an easy way to get cash fast, missing even one payment puts your car at risk of repossession. Without reliable transportation, attending classes or working becomes difficult.

If you miss a payment, the pawn shop has the right to repossess your vehicle, further exacerbating your financial situation. What started as a quick cash fix could cost you your car. Once repossessed, it’s typically towed to a storage yard or auction lot. At that point, the lender may charge storage and repossession fees, which add to the debt.

Avoiding these products protects your income, credit, and stability, and exploring safer options—like credit unions, payment plans, or financial aid—can prevent a temporary setback from becoming a lasting crisis.